The Fed: One cut and done?

- Sep 15, 2025

- 4 min read

The Fed will almost certainly cut a quarter point this week to 4-4.25% despite inflation still running around 3% and wage growth still too high. But, after this week’s cut, the case for further cuts may prove harder to make.

The market’s focus will be on any changes to the Fed’s rate expectations in its Survey of Economic Projections (SEP) to be provided at this meeting. In June, the last SEP, the median projection for end-2025 was 3.9%, implying one possible further cut this year (with two meetings left). And for end-2026, 3.6%, implying one or two more cuts next year. My guess is that the SEP will be slightly lower this time, but not much, allowing for one further cut this year and leaving the median expectation for end-2026 about the same, close to 3.5%. This is higher than current market expectations. However, the case for any cuts beyond this week depends on inflation behaving better, which is not guaranteed.

GDP growth is a solid 1.5-2%

Last week’s downward revision to jobs growth in the year to last March fuelled more talk of economic slowdown. Growth has indeed slowed but it is too early to talk about a stall, or a recession. Arguably, given the impact of border control in reducing the labour supply, GDP is running close to where it should be – around 1.5-2% at an annual rate. Moreover, the slowdown we have seen may be temporary, caused by tariff uncertainty.

H1 GDP rose at an annualised rate of 1.4%, half the 2024 rate (2.8%). Monthly data confirms the slowdown with indicators from consumer spending to business orders to housing slower this year. The GDPNow estimate for Q3 is 3.1%, which would pull the first three quarters of the year up to 1.9% annualised. Tariffs are a tax still slowly working through but the One Big Beautiful Bill Act provides economic stimulus which may offset them.

Some of the survey data suggest that April/May was the worst time. Surprise, surprise, given Trump’s 'Liberation Day' shock on 2nd April! The impact of that day is clear in consumer confidence and small business data for example, and suggested also by purchasing managers’ indices. Not to mention the swoon in the stock market. But that has been followed by new stock highs over the summer.

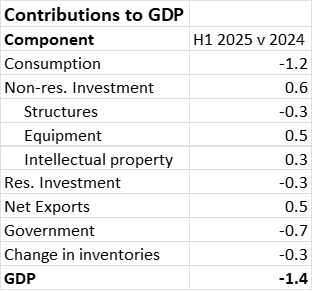

GDP data shows the slowdown is due to consumers and government

A quick look at the details of the GDP data, averaging the first two quarters and comparing with 2024 is useful (see table). Consumer spending contributed 1.2% less to GDP in H1 as consumers held back. The government contributed 0.7% less, swinging from adding 0.6% in 2024 to subtracting -0.1% in H1. Other smaller declines were in structures, housing investment and inventories. There were significant increases in contributions though from investments in equipment and intellectual property, much of it likely linked to AI, and also net exports – the latter reflecting lower imports, likely due to tariffs.

Does slower jobs growth matter?

The latest revisions to jobs show slightly less than half as many were created in the year to last March than earlier reported. But that is history. What is important is that jobs growth in the last three months is running lower than last year’s levels. It is hard to tell how much this is due to reduced availability of labour, caused by immigration control and how much due to employer caution over hiring caused by tariff uncertainty. If it is the latter, we could see payrolls pick up over the next few months if firms become more relaxed about tariffs.

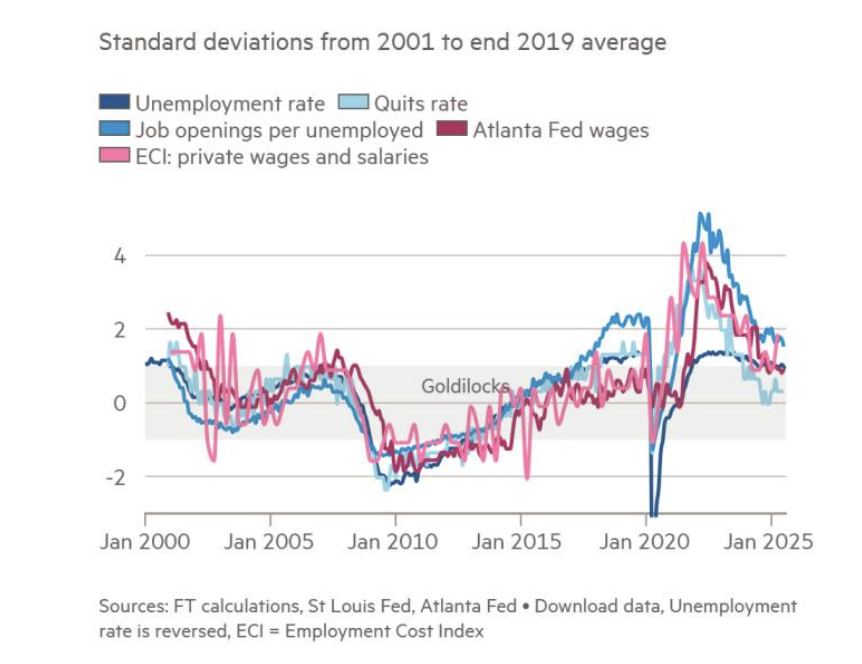

Although jobs growth has weakened, most indicators of the state of the labour market suggest it is still fairly robust. The chart below from the Financial Times shows several different indicators, measured in terms of standard deviations from their average over the last 25 years. Plainly, the labour market has eased since the very tight conditions in 2022. But a quick glance shows that it is broadly comparable to 2000, 2007 and 2019, all periods when the labour market was strong.

Good news on inflation?

If economic growth continues at a 1.5-2% rate, only surprisingly good news on inflation seems likely to tip the Fed heavily towards further rate cuts. We didn’t have that from the CPI last week, though markets cheered because it wasn’t worse than expected. But most inflation measures suggest inflation has stuck at around 3%. And the Atlanta Fed Wage Tracker, the best indicator of wage growth also seems to have stuck, at just over 4%. It is only slightly too high at that rate, maybe 0.5% or so, but unless productivity growth is strong, it is not consistent with 2% inflation. Moreover, if GDP growth is too strong and labour force growth is limited, there is a risk that wage growth starts to rise again. Further rate cuts may have to wait for better news on inflation, which may or may not be coming.

Comments